At 42, sitting in my Bengaluru apartment, I often catch myself wondering: What does financial freedom really mean for someone like me? I have no debt, but also no savings to boast of. I have a wife, a 12‑year‑old daughter, and the usual rhythm of life in a Tier 1 city — groceries, LPG cylinders, internet bills, petrol for long drives, and dreams of family vacations.

Financial freedom, for me, isn’t about luxury. It’s about peace of mind. It’s about knowing that my daughter’s education is secure, our health is protected, and we can live a moderate life without the constant fear of “what if.”

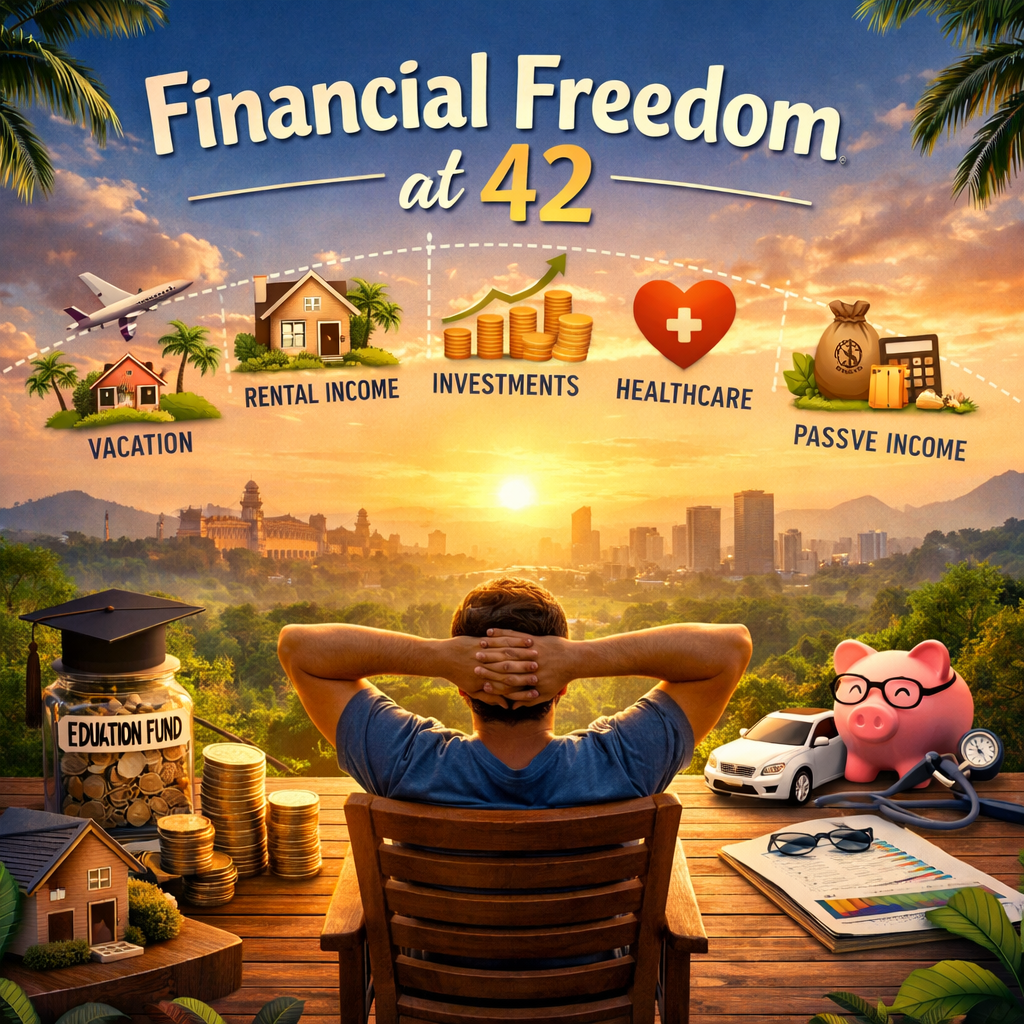

🧩 The Picture of Freedom

When I imagine freedom in Bengaluru, it looks like this:

- Child education: My daughter’s engineering degree, a promise I want to keep.

- Household basics: Groceries, LPG, internet, electricity — the everyday essentials.

- Transport: Petrol for ~15,000 km a year, including those long drives to Coorg or Ooty.

- Healthcare: A family floater policy and an emergency buffer.

- Vacations: 2–3 trips within India, because memories matter more than possessions.

📊 Counting the Costs

Living in Bengaluru isn’t cheap. Here’s what a moderate life adds up to:

| Expense Category | Annual Estimate (₹) | Notes |

|---|---|---|

| Groceries & utilities | 4–5 lakh | Tier 1 city costs |

| Transport | 2.5–3 lakh | Petrol + servicing |

| Healthcare | 1.5–2 lakh | Insurance premium + out-of-pocket |

| Vacations | 2–3 lakh | Domestic trips |

| Child education | 15–25 lakh (one-time) | Spread over 4 years |

| Miscellaneous buffer | 1–2 lakh | Clothing, festivals, emergencies |

👉 Annual living cost: ~₹10–12 lakh (excluding education lump sum).

🚀 The Freedom Corpus

To sustain this lifestyle without a job, I’d need:

- Emergency fund: 6–12 months (~₹12 lakh).

- Education fund: ₹15–25 lakh earmarked separately.

- Freedom corpus: Enough to generate ₹10–12 lakh/year passively.

Using the 4% withdrawal rule:

Corpus = 12,00,000 / 0.04 = approx 3 crore

That’s the target corpus for financial freedom in Bengaluru.

🛠 My Action Plan

- Invest aggressively: Equity mutual funds + index funds for growth.

- Diversify: Debt instruments (PPF, bonds, FDs) for stability.

- Insurance: Health + term life to protect family.

- Track expenses: Avoid lifestyle inflation, stay disciplined.

💡 Passive Income Streams I Dream Of

Financial freedom isn’t just about saving — it’s about creating streams of income that work while I sleep. Here are some ideas I’m exploring:

- Rental income: A small flat or commercial property in Bengaluru’s IT corridors.

- Dividend stocks: Companies that reward shareholders regularly.

- Digital products: E-books, online courses, or templates.

- Freelance consulting: Leveraging my professional expertise part-time.

- Systematic withdrawal plans: From mutual funds once corpus is built.

- Side business: A café, franchise, or online store — scalable with minimal daily involvement.

✍️ Closing Reflection

At 42, in Bengaluru, financial freedom is not a distant dream. It’s a clear, disciplined plan: build a corpus, secure education, protect health, and create passive streams.

Freedom isn’t about age. It’s about clarity, discipline, and the courage to start today.

Leave a comment